New research from the latest Omdia Public Displays Market Tracker has found public display shipments have reduced in 4Q23 to 1.37 million compared to the previous quarter at 1.62 million. This decrease stems from reduced demand across all product categories, particularly evident in IFP/touch display shipments, which experienced a significant 26% decline quarter on quarter (QoQ). This quarterly decline has had a notable impact on the overall public display market as IFP/touch display holds 45.2% of the market share.

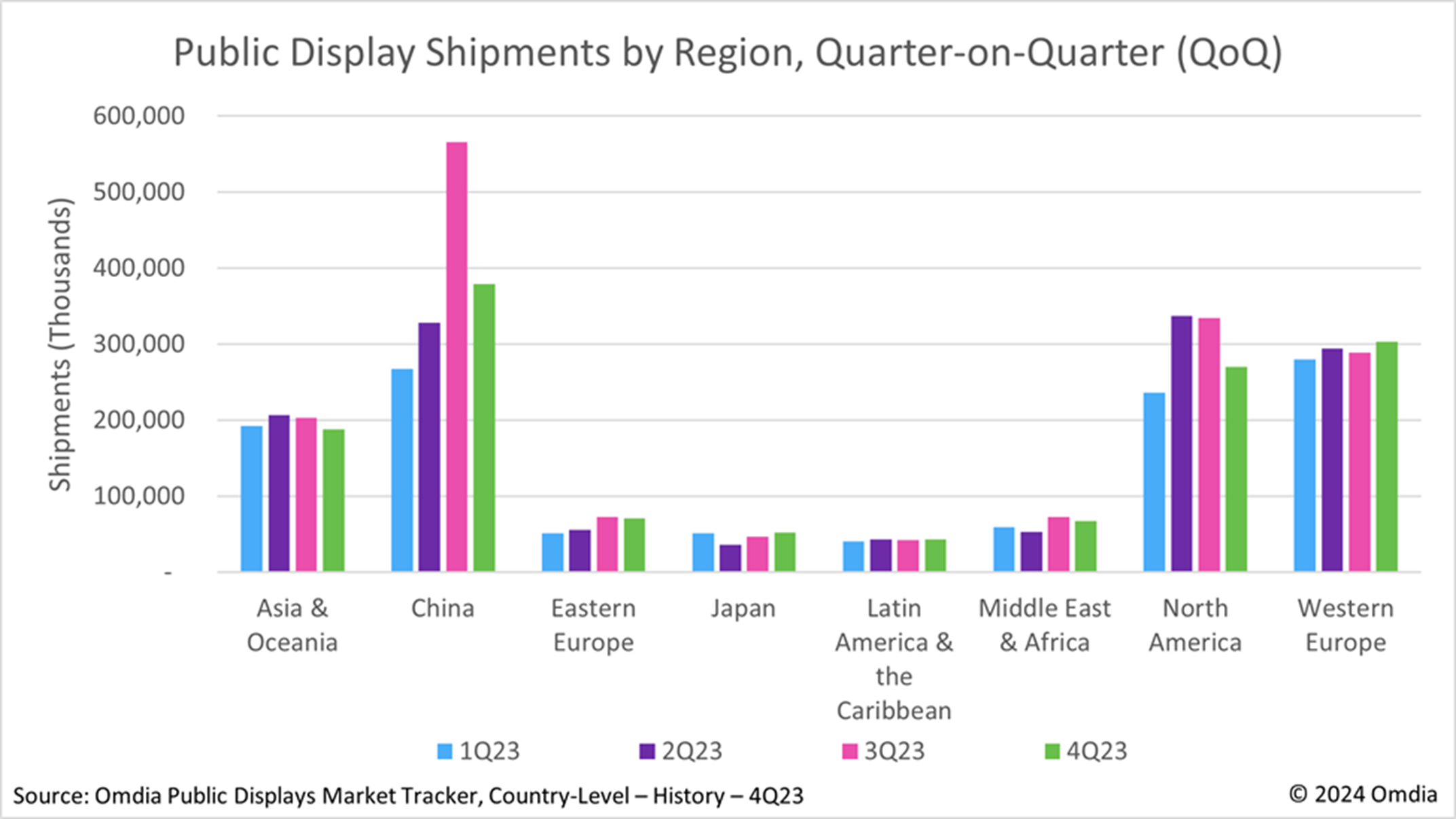

Despite Western Europe's quarterly growth in of 4.8% QoQ in 4Q23, this increase could not offset the impact of North America's and China's performance. North America's and China's weaker than anticipated performance led to both regions recording double-digit quarterly declines in 4Q23. Public display shipments in China dropped to nearly 379,000 units (3Q23: 566,197 units), with declines largely coming from IFP/touch displays and video wall categories. China's enterprise and corporate sectors were impacted by layoffs, budget cuts, and reduction in operating expenses with recovery relying heavily on overall economic conditions. In 4Q23, North America recorded slightly over 270,000 units (compared to 335,017 units in 3Q23) marking a 19.3% decrease QoQ. This decline is attributed to ongoing economic uncertainties in the region, leading to postponed project timelines in both the corporate and education sectors.

Asia & Oceania also endured a similar downtrend with a 7.2% QoQ decline in public display shipments, translating to just over 188,000 units shipped, the lowest since 1Q23 (193,000 units). The region's largest market, India, recorded a mere shipment number of 88,000 after boasting three consecutive quarters of growth before 4Q23.

Despite the ongoing property crisis in China, the region is expected to experience a degree of economic recovery largely due to its government's additional financial aid. This aid is primarily aimed at bolstering infrastructural developments slated for implementation throughout 2024. Potential growth may stem from subsidized loans intended to support industry digital transformations that focus on data visualization and production process monitoring.

As for North America, inflation rates in the U.S. are anticipated to improve in 2024 compared to last year, which may allow for a stronger second half in2024. The labor market continues to fluctuate with continued layoffs in the technology sector in certain states, but the overall labor market remains tight. Other factors may affect the region's economic growth this year, including the upcoming election and geopolitical tensions in the Middle East.

In Asia & Oceania, India continues to be the exception of economic uncertainty as the country, along with its ASEAN counterparts look to capitalize on high volumes of export trade, industrialization, and international tourism activities.

Kelly Lum, principal analyst with Omdia's ProAV practice, commented: "Aside from the various economic impacts in different regions, Omdia expects growth in 2024 for the overall ProAV sector to be driven by interactive touch displays and their expansion in opportunities within the corporate sector for increased collaboration and video conferencing for hybrid work. Ultra-wide large format LCDs also offer additional potential for expansion in the enterprise and corporate sector as well, with many display vendors focusing on these types of products."